The Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (the Act) is changing.

If you're a real estate professional in Australia, you may be hearing about “Tranche 2" and wondering what it means for your business. Tranche2 refers to major changes to Australia's Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) regulations that will be applicable to all real estate agencies from July 2026.

The reforms are expected to bring about a substantial shift in how your agency approaches risk management and operational processes, including client onboarding. For real estate professionals, preparing for these new obligations is essential to ensure compliance and avoid severe penalties.

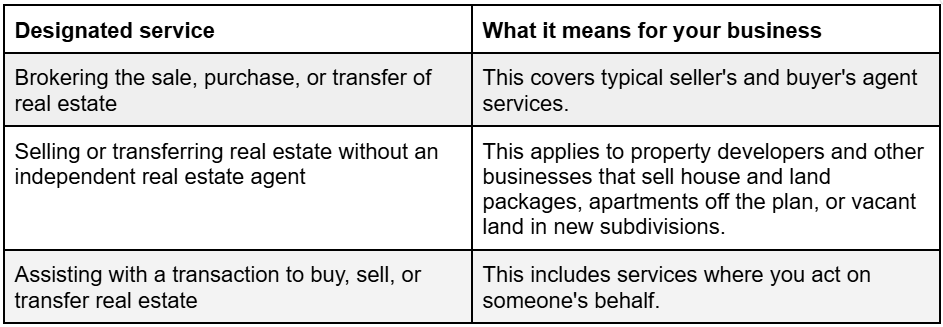

If your real estate agency provides one or more of the following ‘designated services’, the AML/CTF regulations will apply to you:

Why are AML/CTF reforms happening?

Australia's existing AML/CTF laws, drafted in 2005, have not kept pace with the evolving tactics of serious and organised crime. This regulatory gap has allowed criminals to exploit legitimate businesses to launder money, which often funds further illicit activities.

The Tranche 2 reforms will close this gap, bringing Australia in line with international standards set by the Financial Action Task Force (FATF). This is a critical step to ensure Australia can effectively deter, detect, and disrupt financial crime.

Who is impacted?

The compliance net is broadening significantly. While AML/CTF compliance has previously been limited to approximately 19,000 reporting entities1, primarily from the banking and financial services sector, the new reforms will bring in an additional 90,000 entities2. This new group of regulated professionals includes:

- Lawyers and conveyancers

- Real estate professionals

- Accountants

- Virtual Asset Service providers (e.g., digital currency exchanges)

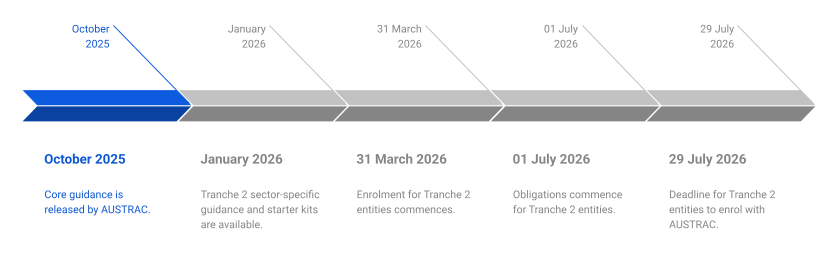

- When do real estate professionals have to comply?

-

The rollout of the Tranche 2 reforms is staged, with key deadlines you need to be aware of:

What will compliance look like for my real estate agency?

The reforms shift the focus of AML/CTF to a risk-based, harm-prevention model. AUSTRAC, the financial intelligence and regulatory agency, will be looking to see that you are taking meaningful action to prevent financial crime.

Early preparation and a focus on simplicity are essential to ensure your AML/CTF program is effective and not overly costly. The core obligations you will need to implement include:

1. Enrolment with AUSTRAC

Your real estate agency must register with AUSTRAC by 29 July, 2026. Your obligations will commence on 1 July 2026.

2. Conduct a risk assessment

This is the foundational step. A thorough risk assessment of your practice will pinpoint potential vulnerabilities and develop a clear understanding of your exposure to money laundering and terrorism financing.

3. Develop an AML/CTF program

The Tranche 2 reforms provide flexibility to develop a program tailored to your firm’s specific risks, size and complexity. It must, however, include key policies and procedures for areas like customer due diligence, transaction monitoring, and reporting - all designed to prevent financial crime and show that your firm is focussed on meaningful outcomes, not just on process.

4. Customer Due Diligence (CDD)

You must identify and verify the identity of individual clients and beneficial owners, and understand the risk they pose, before providing a designated service.

5. Ongoing Customer Due Diligence (OCDD)

Due diligence doesn’t stop after onboarding. You must continue to monitor client relationships over time to detect changes in behaviour and transactions. Any change to the risk profile of the client must trigger the appropriate due diligence checks.

6. Enhanced Customer Due Diligence (ECDD)

A deeper level of due diligence is required for high-risk clients, including Politically Exposed Persons (PEPs) or transactions with no apparent economic or legal purpose.

7. Reporting

Your firm will be required to report certain transactions and any suspicious activity to AUSTRAC.

8. Record keeping

You must maintain a full audit trail of your compliance activities, including records of customer identification, transactions and your AML/CTF program.

Source: Equifax